The financial services industry is a dynamic and ever-changing landscape. The current speed of change has one record that breaks all others: the speed at which customer expectations are changing. Customers demand nothing but immediate payments. This is where Real-Time Payments (RTP) and Open Banking solutions come into the equation. These solutions are about to change the way money is sent, and the way data related to money is used.

What Are Real-Time Payments?

Real-time payments (RTP) enable the immediate transfer of funds from one bank account to another, with the confirmation or settlement of funds happening almost instantly. Compared to the traditional payment process, which uses batch processing and involves the clearing cycle taking several cycles to complete, the RTP process runs on an ongoing, 24/7/365 basis so that the funds will be immediately available to the payee. For businesses, the acceleration of transfer presents an opportunity to optimize cash flow management, simplify administrative processes and create a more seamless customer experience.

Common Use Cases

- Peer-to-Peer(P2P): Immediate transfer of funds to friends or family.

- Business-to-Business(B2B): Immediate payment of an invoice.

- Business-to-Consumer(B2C): Instant payroll, Insurance payouts, reimbursement

- Consumer-to-Business(C2B): Immediate utility bill payments, retail purchases.

According to a report by ACI Worldwide and Global Data, real-time payment transactions are projected to grow by 63% annually to reach a total of US$511 billion per year by 2027. From the speed of e-commerce transactions to the real-time payout of gig economy workers, instant transactions have the potential to alter many different aspects of commerce.

A successful example of real-time payment on a global scale would be the Unified Payments Interface (UPI) in India, which is the biggest real-time payment system in the world. It allows people to transfer funds between banks with the help of just a phone and a virtual payment

Open Banking Revolutionizing Financial Innovations

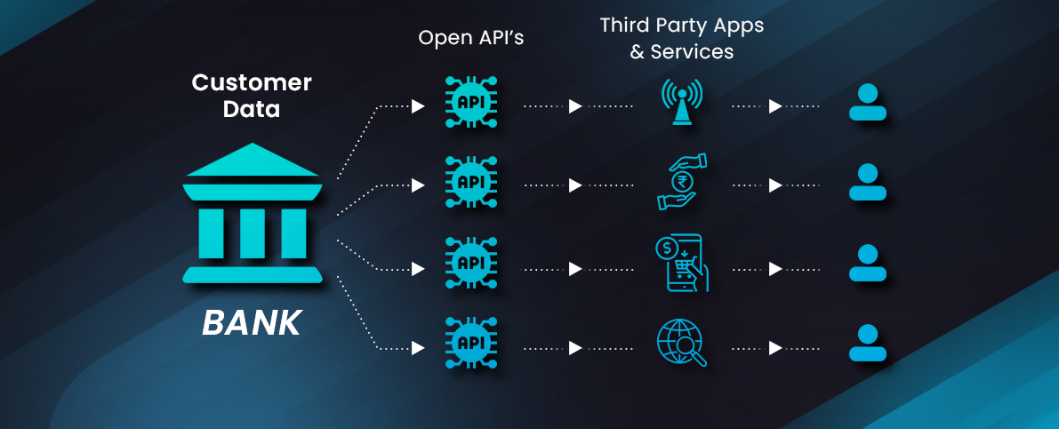

Open Banking is transforming financial services by using secure APIs to allow 3rd party providers (TPPs) to access consumer financial data with consent, fostering innovation and competition. Open Banking represents a new phenomenon that has intervened in the manner in which financial data is provided. It is, in fact, a secure sharing of financial information with third-party developers, as well as fintechs, with their consent, through API. This model breaks the data silos, so that fintechs, as well as financial institutions, can access the data, including making payments directly.

Open Banking enables the creation of new services that can be delivered through a far more interoperable finance system, including services such as a personal finance aggregation platform, savings applications, or payment initiation services. The convergence of Open Banking and real-time payments means fast payments with smart and data-driven insights.

How These Technologies Enhance Customer Experience

- Instant Gratification and Convenience

Real-time payments mean that the waiting time for transactions no longer remains a fact. Whether it is making a payment at a merchant, paying friends, or getting a refund, the modern-day customer expects instant confirmation and instant access to their funds, which is a major satisfaction enhancer. - Enhanced Financial Management and Personalization

The customers can manage their data using Open Banking. Customers can give third-party apps access to their spending behavior so that the apps can give them advice on how they can save their money better. This is not possible in the traditional banking system. - Seamless Omnichannel Experience

By linking APIs and real-time processing, companies are able to provide smooth checkout experiences, lower transaction costs, and access real-time balance information, so that a smooth journey can be provided across various platforms.

Future Prospects

Looking ahead, the future for real-time payments and Open Banking is even more integrated than it is today as payment innovation enters an exciting period with the introduction of a plethora of new payment solutions such as voice payment services, AI financial tools, and the next-generation payment experiences for the desktop and IoT segments.

What this means for BFSI is not only upgrading infrastructure but also thinking about how products are built, delivered, and experienced, to create services that delight consumers and build trust in digital finance ecosystems.

Shuvankar is a Business Analyst with 18 years of experience supporting BFSI and financial services organizations in digital transformation, process improvement, and product enhancement. He works closely with senior stakeholders to translate business objectives into operating models and technology-driven solutions for lending and leasing platforms.

His work covers business analysis, gap and impact assessment, regulatory-aligned solution design, and delivery through Agile and hybrid models. At Happiest Minds Technologies, he supports global customers in improving finance operations with measurable business outcomes.